INVESTMENTS / Published: September 2024

NYSE: OXY

The oil and gas industry is cyclical. During periods of rising demand, companies increase capital expenditures to capitalize on higher profits, leading to supply saturation and eventually driving prices down. When demand contracts, profits and spending collapse, triggering a wave of consolidation. This consolidation then creates new opportunities for expansion, and the cycle begins anew.

This business model can often seem like a game of predicting macroeconomic trends rather than a sound investment strategy. However, a company that breaks out of this cycle and manages its capital wisely through booms and busts has an opportunity to capture value in the margins. This flexibility isn't available to companies still in their growth phase, as they often need to spend heavily on exploration which exposes them to difficult decisions where every move must be precisely timed.

In contrast, a company that has already navigated these challenges and can capitalize on its fields without significant exploration costs can generate cash flow from a commodity essential to civilization, with limited downside risk. If such a company exists and its management is committed to returning cash flow to shareholders - through dividends or share buybacks - it could be an ideal investment as it would become a highly predictable cash-generating machine, offering a risk/return profile that surpasses most bonds in the market.

Occidental Petroleum’s earnings call for Q2 2022:

Question: I appreciate the answer, Vicki. And I'm going to stay with you, if I may, as a quick follow-up. So before things got crazy over the last couple of years, you had talked about low single-digit growth in production. And of course, the priorities all changed with the balance sheet. So as you kind of get line of sight to the balance sheet and back to perhaps where you want it to be, what are you thinking now in terms of what happens to the growth element of prioritizing in terms of where you relatively prioritize capital? And I'll leave it there.

Answer: Well, the good thing is what we see that we have today is a great opportunity, and that is that we don't have to grow our cash flow right now. And we have an opportunity because of the valuation of our stock right now to continue to make that a key part of our value proposition going forward. We'll do a little bit of dividend increase. We'll certainly mature our debt faster than what the current schedule is in terms of maturities because we want to accelerate that. But we'll also buy back a significant volume of shares, or at least we hope to over the next few years. And we don't feel the need to grow production until we get beyond that point because we feel like one of the best values right now is investment in our own stock.

From the above statement, it can be assumed, one, that the cash flow will be returned to shareholders, two, they will focus on solidifying the cash flow instead of expansion of operations. As a result, it is reasonable to expect that the free cash flow yield will effectively translate into return per share.

At a share price of $60, with a WTI price indexed at $77, OXY's 2023 free cash flow yield stands around 9%.

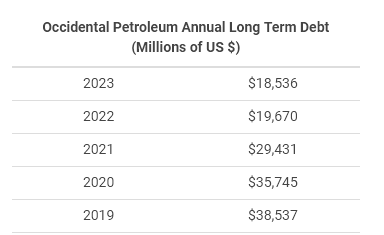

OXY is also in the midst of a debt reduction program - accrued by CrownRock acquisition, aiming to bring debt down to $15 billion. Achieving this target is expected to add, conservatively, $1 billion to their free cash flow.

Moreover, OXY’s industry-leading carbon capture technology, combined with the expansion of OxyChem - specifically Project Redstone and other minor initiatives, is likely to contribute, conservatively, an additional 5% to free cash flow over time.

Considering the ESG-driven under-investment in the oil sector and the underestimated demand for oil, it is probable that oil prices will remain above the lows seen during the COVID-19 era. Even in a low oil price environment, OXY's strategy of returning cash flow to shareholders rather than aggressively expanding operations will help maintain attractive per-share yields. For instance, with WTI prices below $40, OXY still generates about $2 billion in free cash flow, yielding around 3% at $60 per share.

With a current free cash flow yield of 9%, modest growth in cash flow, and limited downside risk from falling oil prices, OXY appears to be an attractive investment, potentially serving as an alternative to any kind of bonds in the market.